The Market Mosaic 5.5.24

Dovish Fed? Follow these 3 charts to track risk sentiment.

Welcome back to The Market Mosaic, where I gauge the stock market’s next move by looking at macro, technicals, and market internals. I’ll also highlight trade ideas using this analysis.

If you find this content helpful please hit that “like” button, share this post, and become a subscriber to this always free report if you haven’t already done so!

And be sure to check out Mosaic Chart Alerts. It’s a midweek update covering chart setups among long and short trade ideas in the stock market, along with levels I’m watching.

First, a quick message:

I want to make sure you can find my updated thoughts and analysis on trade ideas.

Using Substack’s Chat feature, I’m posting about the setups I cover in The Market Mosaic and Mosaic Chart Alerts that are breaking out and meeting my criteria for taking a position.

I’ll highlight various aspects of why the breakout meets my process for adding a trade, and how I plan to manage a position including stop losses.

But I’m honestly not sure if you’re monitoring the Substack Chat feature, so I wanted to make sure you’re able to access it.

You’ll need Substack’s app, which you can get by clicking this link. Substack Chat should work on both iOS and Android.

Simply go to the Chat feature on the app if you want to follow along…I look forward to seeing you there!

Now for this week’s issue…

A weaker than expected jobs report and signs of cooling economic activity delivered relief for investors.

Following last week’s rate-setting meeting, Federal Reserve Chair Jerome Powell stressed that the central bank needs to see inflation fall further to their 2% target before cutting interest rates.

But Powell also hedged that outlook by stating that “unexpected weakening in the labor market” could provide an avenue for rate cuts even if inflation remains highs.

So when the payrolls report for the month of April showed 175,000 jobs created for the month (chart below) versus expectations for 240,000, stocks rallied in response. The Dow Jones Industrial Average rose added 450 points, while the Nasdaq gained nearly 2% on the day.

That’s because a weaker than expected jobs report put the prospect of rate cuts back in the picture. Market-implied odds now point to a cut at the Fed’s meeting in September, and shows two cuts on the year compared to one going into the jobs report.

Other leading indicators of monetary policy are reversing course as well. After briefly moving over the 5% level (arrow) following a breakout from an ascending triangle pattern in the chart below, the 2-year Treasury yield is pulling back to 4.8% which is 0.53% below the current effective fund funds rate (or worth about two 0.25% rate cuts).

But investors won’t have to wait for rate cuts to see a dovish pivot by the Fed. Also in last week’s meeting, the Fed announced that the balance sheet runoff will start slowing. That’s where government bonds acquired as part of the Fed’s quantitative easing program are allowed to mature, which has brought the Fed’s balance sheet assets down to $7.4 trillion from nearly $9 trillion at the peak in 2022. But the Fed will reduce the pace of Treasury maturities to $25 billion from $60 billion starting in June.

Even with the dovish shift, it’s interesting to note that financial conditions overall remain looser than average in the chart below (under zero indicates conditions are looser than the historical average). I look at financial conditions as the cost and availability of credit, where cheap and easy access is historically a positive tailwind for asset prices.

If new developments on the outlook for monetary policy loosen financial conditions further, that should help get the stock market rally back on track. And if that’s the case, I would expect the more speculative corners of the capital markets to respond favorably as well.

Here are the charts and key levels I’m watching to suggest if the rally unfolding since mid-April is a dead cat bounce or if the bull market is getting back on track.

Risk Sentiment: The Good, the Bad, and the Ugly

Loose financial conditions should be boosting speculative sectors and asset classes. Those tend to be the most sensitive to credit and liquidity conditions, like what you saw in the liquidity-driven boom and bust period from 2020/2021 and into 2022’s bear market. Just take a look at the Ark Innovation ETF (ARKK) from this period to see my point.

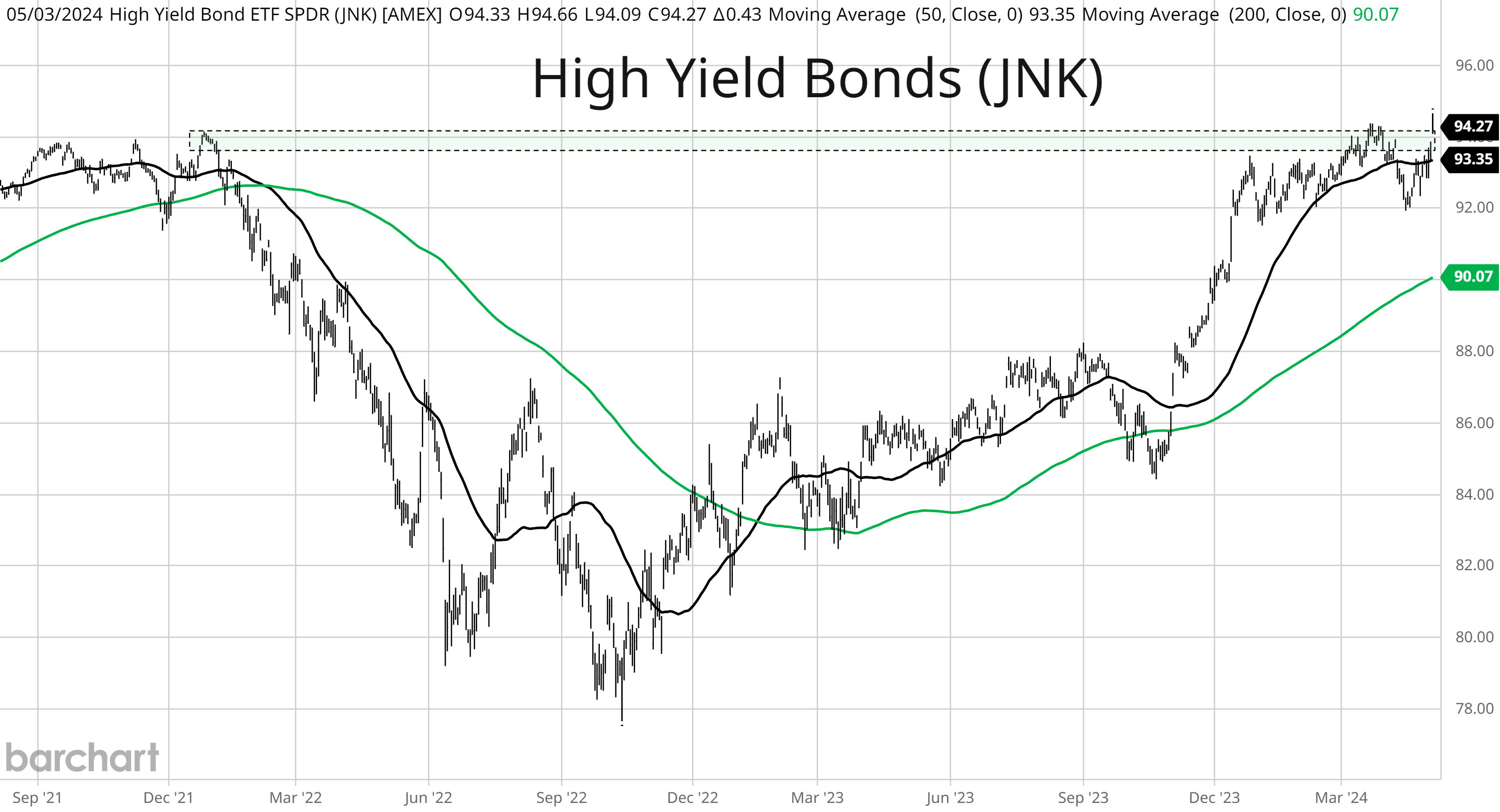

In that regard, some charts are looking better than others. I’ll start with high yield bonds, where I track metrics like spreads relative to safer fixed income securities (like Treasuries) and the performance of various high yield categories. I also follow the total return indexes and their related exchange-traded funds (ETFs) for key levels and important breakouts or breakdowns.

Companies issuing high yield debt are already on shaky financial ground, which makes the performance of high yield debt very sensitive to changes in the economic outlook. That’s why the SPDR High Yield Bond ETF (JNK) breaking out to new highs is the most bullish thing I’ve seen all week, which you can see in the chart below.

I took this chart back to the end of 2021 so you can see the prior high. That high was tested recently in late March before JNK turned lower, which was also a warning flag for the S&P 500 that peaked about a week later. But a strong rally since mid-April is now leading JNK to breakout to new all-time highs.

But this past week saw Bitcoin flashing some bad price action, at least until Friday. I’m not a crypto expert, but I will note that Bitcoin has a history of anticipating key turning points in the stock market. That makes it useful for tracking risk sentiment and the mood of investors.

Like when Bitcoin peaked ahead of the S&P 500 last July, or when Bitcoin found a bottom last September ahead of the S&P’s bottom in late October. More recently, Bitcoin peaked in mid-March (circle) several weeks before the S&P. That makes last week’s action concerning, with Bitcoin making another "lower low" (arrow) off the March peak as you can see below.

Bitcoin did recapture the breakdown level late last week. But for me to consider that a bullish change in trend, I want to see price recapture the 50-day moving average (MA - black line) and the $67,000 level. Otherwise, Bitcoin still in a downtrend since it made a lower low and lower high on this pullback.

The ugly belongs to small-cap growth stocks. Due to the interest rate impact on valuations (because future profits are discounted back to today’s present value) and since small-growth companies tend to see most of their profits far off in the future, they are extremely sensitive to the rate outlook and changes in financial conditions.

And if there’s one fund flashing a bearish pattern, it’s the IWO exchange-traded fund that tracks the Russell 2000 Growth Index. You can see IWO is potentially creating a bearish “head and shoulders” pattern in the chart below.

The current price action is coming up to test the 50-day MA while the MACD is resetting below the zero line and RSI coming up to the 50 level. If price momentum turns back lower and IWO moves below neckline support around $245, that will complete the bearish setup.

How these chart patterns play out will reveal if the prospect for looser financial conditions can be a tailwind for asset prices. If we see reversals in areas like high yield or a bearish breakdown in small-cap growth, that points to a more concerning development on the horizon.

Now What…

While the knee-jerk stock market reaction to Friday’s payrolls report was positive, investors don’t want to see weaker economic data persist for too long.

Although evidence of a slowing economy may ultimately push the Fed to cut interest rates, stocks tend to follow earnings over the long-term. And if/when the Fed does start cutting interest rates, the path of stocks ultimately comes down to whether or not the economy avoids a recession which you can see in the chart below.

The red line shows the S&P 500 performance once the Fed starts cutting and the economy enters recession. The green line is when rate cuts occur with no recession. That again highlights the impact of corporate earnings on stock prices.

Plus falling interest rates on the short-end (induced by monetary policy) doesn’t automatically translate to higher stock prices. In fact, some of the worst bear markets in history took place when the Fed was rapidly cutting interest rates. The chart below shows the effective fed funds rate (blue line) compared to the Wilshire 5000 Price Index (red line) that tracks the stock market. You can see that major bear markets from 2000 and 2008 coincided with rate cuts by the Fed, which were episodes marked by recession.

While recent weakness in some economic reports should not be a welcome sign, I wouldn’t read too much into a single month’s data point with things like payrolls or the 1Q GDP report. Even JPMorgan CEO Jamie Dimon described the U.S. economy as “booming” less than two weeks ago.

In addition to watching how the charts above indicate shifting views around risk-taking sentiment among investors, I’m still watching breakout setups across several sectors that should benefit from a strong economy and demand-induced inflation.

For example, I have a hard time being bearish on the economy when a copper mining stock like Freeport-McMoRan (FCX) is breaking out to its highest level ever that you can see with the FCX monthly chart below going back to 2007. The stock is moving out of a symmetrical triangle pattern going back to 2022 just as the monthly MACD is turning higher from the zero line.

And leadership from stocks in industrial sectors is not something you tend to see if a recession is around the corner. We’re recently tracking the breakout in an industrial chart setup with Itron (ITRI). After breaking out over the $100 level on a jump in volume and the relative strength line at new 52-week highs, the stock could test the prior highs around the $120 level. It’s also worth noting that the company grew earnings per share by 197% last year, while earnings are expected to increase another 19% this year.

That’s all for this week. The coming week will be light on economic data but will feature several speakers from the Fed in the aftermath of the latest rate-setting meeting. While investors will be looking for more clues that a dovish pivot could be underway, the performance in the capital market’s more speculative sectors will reveal the risk-taking mood of investors and if looser financial conditions can boost stock prices.

I hope you’ve enjoyed The Market Mosaic, and please share this report with your family, friends, coworkers…or anyone that would benefit from an objective look at the stock market.

And make sure you never miss an edition by subscribing here:

For updated charts, market analysis, and other trade ideas, give me a follow on X: @mosaicassetco

And if you have any questions or feedback, feel free to shoot me an email at mosaicassetco@gmail.com

Disclaimer: these are not recommendations and just my thoughts and opinions…do your own due diligence! I may hold a position in the securities mentioned in this report.