The world saw a crisis. The U.S. saw a market.

Plus: 52-year-old dividend stock running tomorrow's AI

Hey Everyone!

I wanted to share a newsletter we’ve been following: Money Machine Newsletter.

It’s designed to help you become a smarter, independent investor with two things:

Market-beating stocks in a 5-min read. Picked by elite traders. Delivered weekly to your inbox pre-market.

Market, investing, and business insights from insiders and experts outside the mainstream media.

You won’t find the same watered down stock picks like other services. Nor will you find the same regurgitated mainstream media information here.

I’ll let Money Machine Newsletter take it from here…

This week’s market, investing, and business insights from insiders and experts outside the mainstream media:

A 300-year-old monopoly just got a wake-up call.

A legacy utility just became the most important backbone in AI.

GPT-5.4 arrives, OpenAI just leveled up again.

THIS company is burning cash to buy your mortgage rate.

And more. Let’s get to it!

Follow us on Instagram | YouTube | X

Top Insights of the Week

1. The world saw a crisis. The U.S. saw a market.

When the Strait of Hormuz gets wobbly, the world holds its breath. And right now, it’s not breathing…

After U.S. and Israeli strikes on Iran, insurance consortiums voided existing war risk policies overnight. The London market’s Joint War Committee expanded the official war zone to cover the entire Persian Gulf. P&I clubs — the mutual insurers that backstop global shipping — announced existing coverage would lapse, requiring entirely new policies for any vessel entering the region. Premiums spiked from 0.25% of a ship’s hull value to 1% — and in some cases as high as 3%. For a $100 million supertanker, that’s a jump from $250,000 to $2–3 million per voyage.

If a shipping company can’t get insurance, their lenders won’t let the boats sail. Simple as that.

Tanker traffic through the Strait dropped 94% — from 50 transits on February 28 to just 3 on March 1. Oil surged to $84 a barrel. This is how inflation starts…

Now, the Strait normally moves about 20 million barrels of oil a day — roughly 20% of global consumption. That flow didn’t just slow down. It stopped. And every day it stays stopped, production across the Gulf backs up. JPMorgan estimates that by eight days of closure, forced production shutdowns could reach 3.3 million barrels per day. Meanwhile, pipeline alternatives through Saudi Arabia and the UAE can only reroute 2.6 to 4.2 million barrels — nowhere near enough.

Most people saw a crisis. Trump saw a market…

The U.S. stepped in. The International Development Finance Corporation announced a $20 billion reinsurance facility for Gulf shipping — hull, machinery, cargo — backed by the U.S. government in coordination with CENTCOM. If the risk is too hot for the private market to price, Washington will backstop it.

Here’s where it gets interesting…

Lloyd’s of London has dominated maritime insurance for over 300 years. And to be fair, Lloyd’s didn’t fully walk away — the Lloyd’s Market Association confirmed on March 5 that it is still quoting war risk insurance and that coverage “currently remains in place” for most vessels in Gulf waters. But it doesn’t matter. The DFC already identified “best-in-class, preferred American insurance partners”. The U.S. government is building the infrastructure to route this business through American firms.

This matters beyond oil. About 90% of Iran’s crude exports go to China. Controlling who insures the ships that carry the world’s energy gives you leverage over everyone who depends on it.

Whether this becomes a permanent reshoring of maritime insurance or just a wartime emergency measure is the real question. Lloyd’s has survived centuries of wars and isn’t going quietly — they’re already in talks with the DFC about a joint public-private arrangement. But the precedent is set. The U.S. government has proven it can step into the insurance game at scale. We’re not just protecting ships. We’re staking a claim on the industry.

2. 52-year-old dividend stock running tomorrow’s AI

Everyone is talking about AI chips. Nobody is talking about the plug. You can’t run a supercomputer on good intentions. You need electricity. Massive, non-stop power. The current grid is tapped out. Renewables are too inconsistent, and nuclear takes a decade to approve. The only scalable fix right now? Natural gas. Enter Williams Companies (WMB)…

They already move a third of all natural gas in the US. They own the pipes. But now, they’re cutting out the middleman.

Instead of just shipping gas, they’re building power plants directly on-site for tech giants. When a massive data center needs power today, Williams routes a pipe right to them, builds a plant next door, and locks in a long-term contract.

They’ve committed $5.1 billion to these direct-to-customer projects, with a backlog expected to hit 6 gigawatts by 2030. It’s an entirely new, highly profitable monopoly.

Market Cap: ~$91B

Forward P/E: ~34x

2025 Revenue: $11.83B

Adjusted EBITDA: $7.75B (targeting $8.20B in 2026)

Dividend Yield: 2.8% (raised for the 52nd consecutive year)

52-week high: $76.87

52-week low: $51.58

The risks…

It’s expensive. Building plants costs real money. 2026 capital expenditures will top $6 billion.

It requires debt. They run at a 4.0x leverage ratio. If interest rates stay sticky, carrying that debt hurts.

It’s regulated. Laying pipe and building plants always means fighting through environmental and political red tape.

Bottom line… Wall Street sees a boring, legacy pipeline. We see the physical backbone making the AI boom possible. Become a premium subscriber and get alerted when this stock triggers our setup for entry point, target price, and stop loss.

Top 3 Charts of the Week

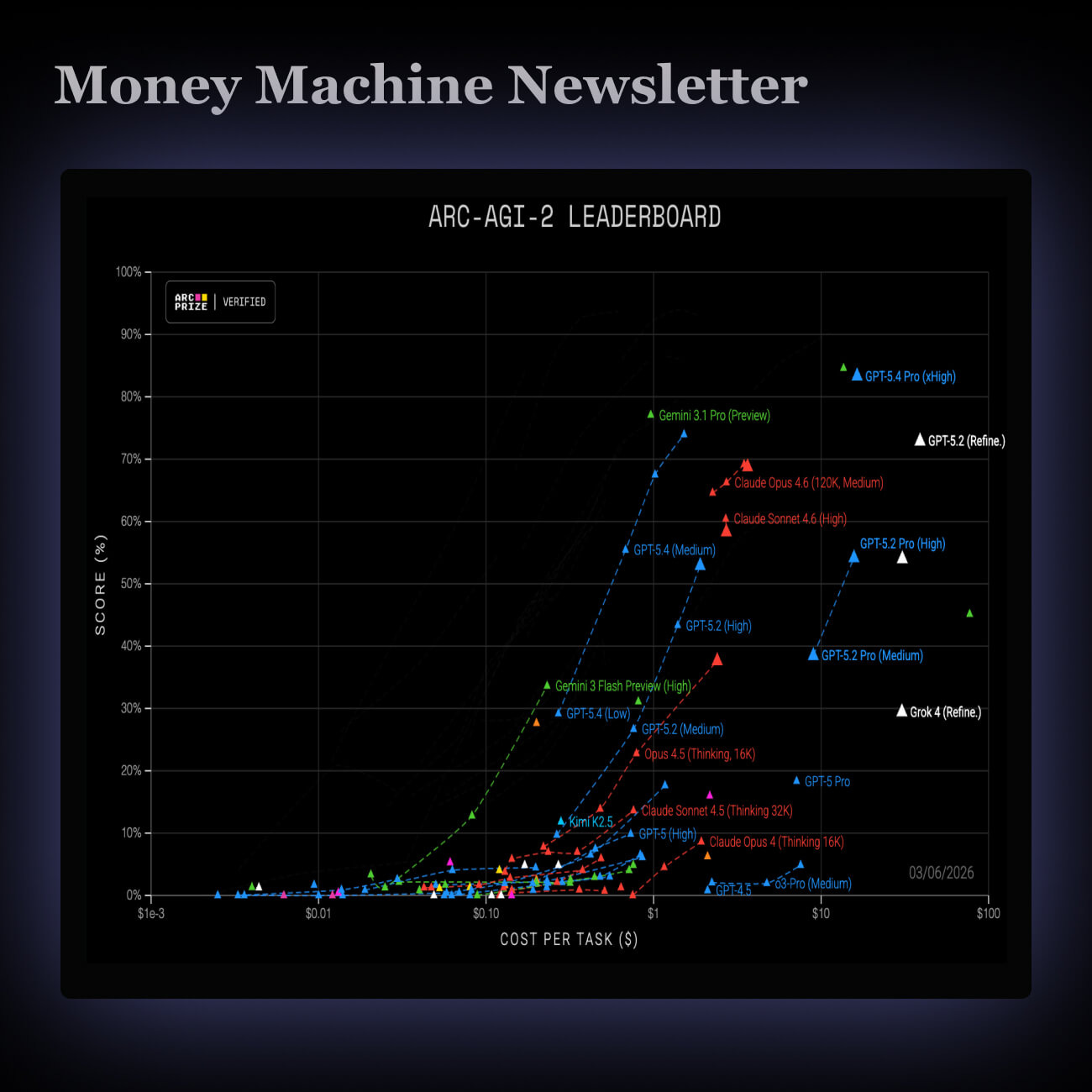

1. GPT-5.4 arrives, OpenAI just leveled up again

OpenAI released GPT-5.4. It’s their smartest tool yet, scoring 83.3% on a big logic test. It’s faster, handles bigger tasks, and even uses your computer for you. It solves harder problems, though it costs more—up to $180 for 1 million tokens.

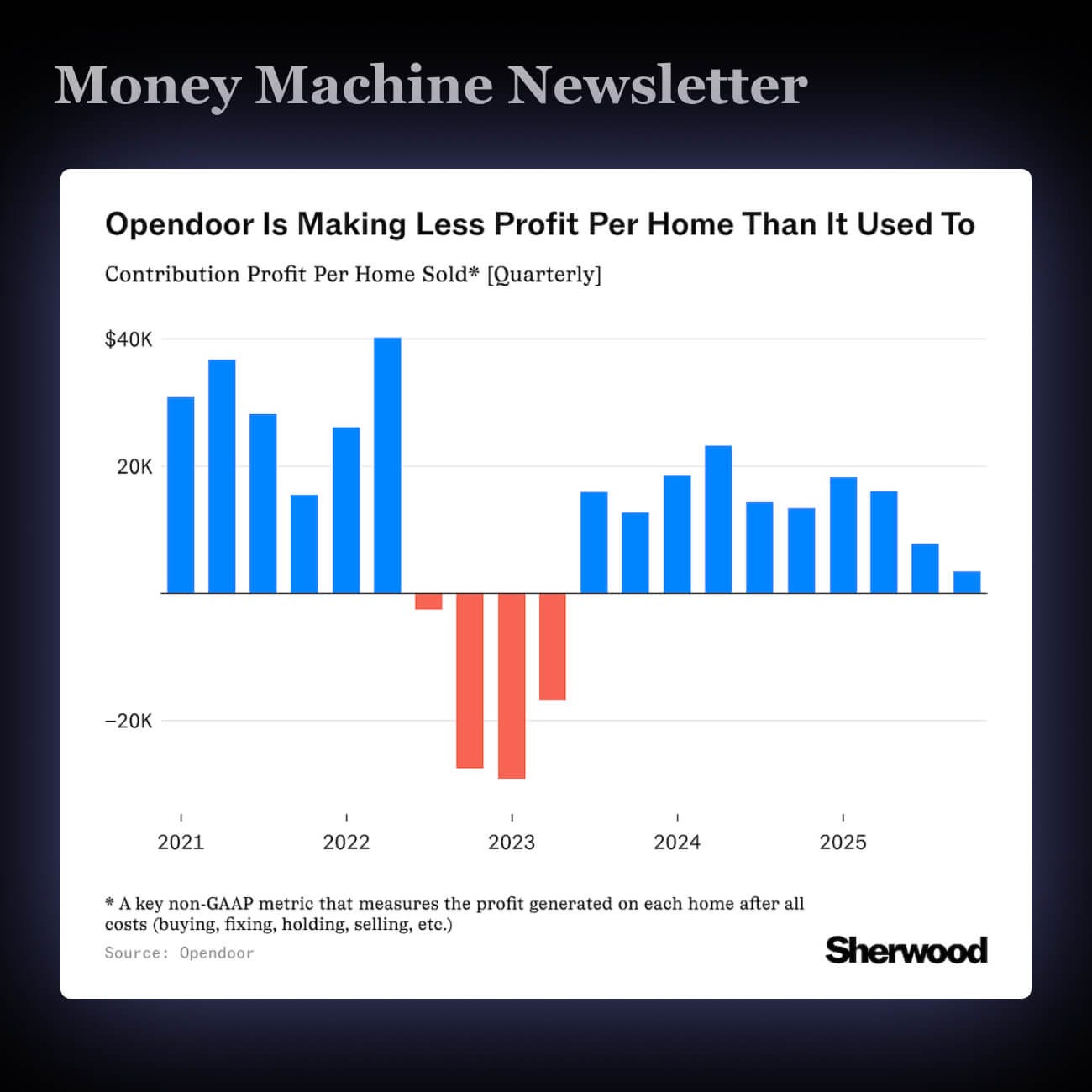

2. Opendoor bets on 4.99% mortgages while its own profits take a hit

Opendoor is offering 4.99% mortgages by cutting out middlemen. They’re losing money elsewhere—net losses hit $1.3 billion—so they’re trying something new to sell houses faster.

They’re using automation to lower rates below the 5.98% average. It’s a gamble to fix their shrinking profit, which dropped from $13,500 to just $3,500 per home.

Buying a house might get cheaper, but the company providing the loan is struggling. If their “new math” doesn’t work, this deal won’t last forever.

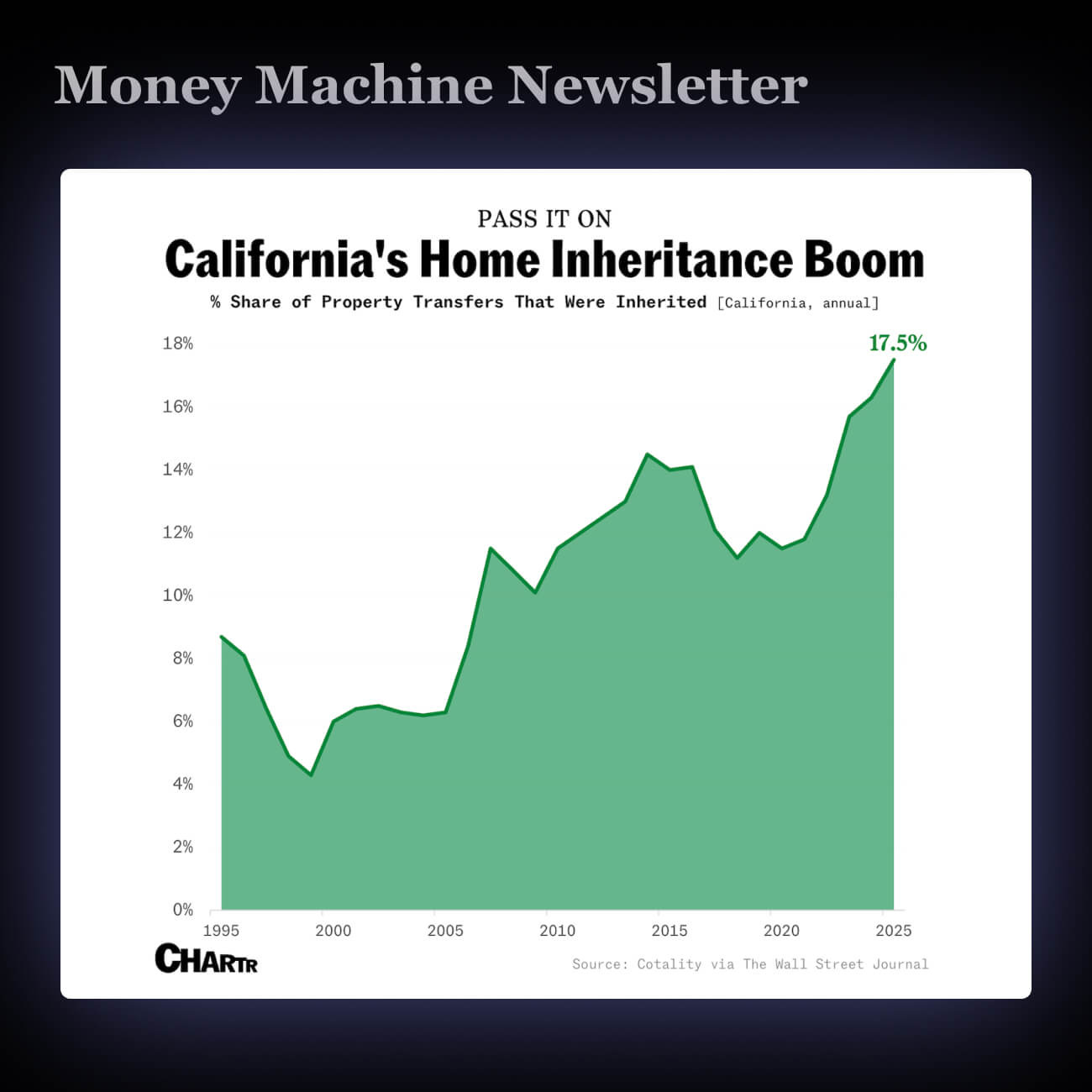

3. 1 in 5 California home transfers are now inheritances

In California, 17.5% of home moves are now inheritances. That’s double the national average and twice what it was thirty years ago.

Buying a house is so expensive that people just wait for their parents’ homes. Low taxes keep families staying put for 20 years. The “California Dream” is changing. Unless you’re born into a house, getting one is harder than ever. It’s a closed loop.

Join 6,000+ self-directed investors who have already placed themselves on the path to greater wealth—potentially making $500, $1,000, $2,000, $3,000, or more every month with Money Machine Newsletter’s trade ideas.

See you in there!

Best,

Money Machine Newsletter

Nothing in this email is intended to serve as financial advice. Do your own research.