The Market Mosaic 7.9.23

3 tailwinds for more stock market gains.

Welcome back to The Market Mosaic, where I gauge the stock market’s next move by looking at macro, technicals, and market internals. I’ll also highlight trade ideas using this analysis.

If you find this content helpful please hit that “like” button, share this post, and become a subscriber to this always free report if you haven’t already done so!

And be sure to check out Mosaic Chart Alerts. It’s a midweek update covering chart setups among long and short ideas in the stock market, along with levels I’m watching.

Now for this week’s issue…

Last week reminded investors that a massive challenge facing the stock market isn’t going away anytime soon…tighter monetary policy.

Lagging measures of the economy, such employment data, remain exceptionally strong. You saw that in various labor market reports. First, the ADP report on private sector payrolls smashed expectations with 497,000 jobs added in June (chart below) which was more than double economist estimates.

The Labor Department’s payrolls report on Friday also confirms a solid job market. Although coming in slightly less than expected, there were still 209,000 jobs added last month while the unemployment rate dipped to 3.6%. That marks the 30th consecutive month of net job additions to the economy.

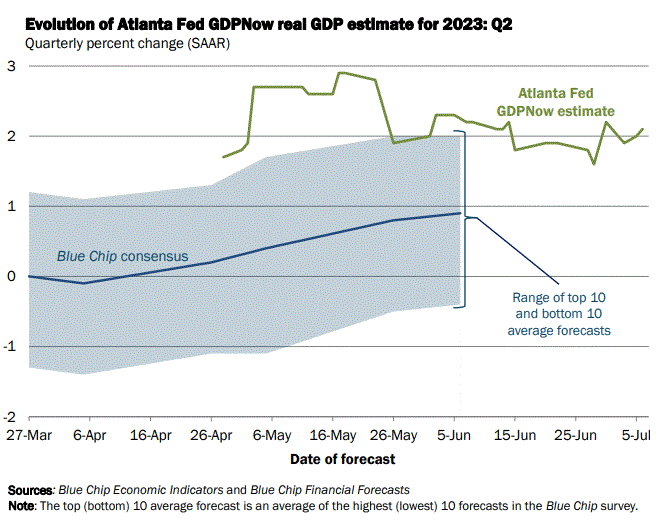

Perhaps then it’s also no surprise that metrics tracking economic growth keep humming as well. The Federal Reserve’s Atlanta district keeps an updated estimate of quarterly GDP growth based on incoming data. It shows Q2 at an annualized rate of just over 2%, which is well ahead of the average economist forecast.

While that all sounds like good news, it means the Fed has a green light to maintain their restrictive policy stance by keeping rates high and shrink their balance sheet via quantitative tightening. The end result is that the Fed continues to drain liquidity from the financial system.

And liquidity is the lifeblood of asset prices, especially speculative ones like stocks and cryptocurrencies.

But despite the ongoing challenges presented by tighter monetary policy, there are conditions in place that could offset the Fed and help boost stock prices.

I’m following these three catalysts that could push stocks higher.

3 Catalysts Driving Demand for Stocks

Corporate earnings drive the longer-term performance of the stock market, which I recently discussed here.

But you shouldn’t lose sight of factors impacting market structure that can drive stock prices over short- and intermediate-term time frames.

And while the liquidity drain by the Fed remains a big concern, there are some offsets at play that could boost demand for stocks in general.

One is with margin debt, especially as investor sentiment becomes more bullish. While I’m not advocating that going on margin to buy stocks is a good idea, it’s still worth tracking this potential source of liquidity and demand.

Margin debt peaked at $935 billion in late 2021, and has now fallen by nearly $300 billion. As a percent of the market’s capitalization, margin debt is at the lowest level since 2004. The chart below shows inflation-adjusted margin debt, its linear trendline, and the S&P 500.

The year-over-year rate of change in margin debt is also hitting levels that have marked a turnaround in the past. The bottom panel in the chart below (h/t Jurrien Timmer) shows the rate of change turning higher from a depressed level, where increases in borrowing could provide a source of liquidity for stocks.

At the same time, there remains a remains a large short position stock index futures that I originally wrote about here in May. After speculators built the largest net short position in S&P 500 Index futures since 2011, they are quickly unwinding that position as you can see in the chart below.

That covering has coincided with a general market rally and improvement in breadth since the start of June. But you can also see that speculators remain in a large net short position, where further covering can be another source of demand.

Back in May, I also discussed how expected volatility levels in stocks can have a significant impact on positioning in risk-parity and other volatility-targeting funds. These strategies operate based on a “risk budget”, and if stock market volatility (i.e. risk) is coming in lower these institutional investors tend to allocate more to equities.

We can track this with the Volatility Index (VIX), which you can see in the weekly chart below going back five years. The dashed line at 20 is the long-term average for the VIX. We’ve mostly been in a higher volatility regime for the past three years. But the recent move under 20 could signal a new lower volatility regime and help draw more institutional flows to stocks.

So while the Fed will remain an obstacle for traders, low levels of margin debt, bearish speculative positioning, and lower levels of volatility could drive new sources of demand for stocks.

Now What…

Participation in the S&P 500’s rally this year has been extremely lopsided, even with broadening breadth since June. While the S&P is now up 14% year-to-date, large cap growth (IWF) is leading the way with a 27% return while large-cap value (IWD) is only up 3%.

Several cyclical sectors like semiconductors, housing, and industrials are performing well. But if the catalysts outlined above can drive more gains, I would like to see value-driven areas of the market respond better.

The chart below shows the Russell 1000 Value ETF (IWD), which tracks large-cap value stocks. You can see price is yet again encountering resistance at a trendline going back to the peak in the ETF. A breakout could signal that value shares are trying to catchup to their growth counterparts.

One value sector seeing a boost this past week has been energy. After lagging for much of 2023, several energy groups are coming to life. Offshore stocks in particular are showing relative strength, where FTI that I highlighted in Mosaic Chart Alerts is holding its breakout.

More recently, I posted about the setup in WFRD and the ascending triangle shown in the chart below. The stock closed just below the $70 resistance level on Friday.

That’s all for this week. This coming week features a barrage of Fed speakers, June’s CPI and PPI inflation reports, and the start of the second quarter earnings season with major banks due to report. While there will be plenty of headlines to toss stocks around, stay disciplined and focus on executing your trade plan!

I hope you’ve enjoyed The Market Mosaic, and please share this report with your family, friends, coworkers…or anyone that would benefit from an objective look at the stock market.

And make sure you never miss an edition by subscribing here:

For updated charts, market analysis, and other trade ideas, give me a follow on Twitter: @mosaicassetco

And if you have any questions or feedback, feel free to shoot me an email at mosaicassetco@gmail.com

Disclaimer: these are not recommendations and just my thoughts and opinions…do your own due diligence! I may hold a position in the securities mentioned in this report.