The Market Mosaic 6.2.24

The bull market can survive “higher for longer”.

Welcome back to The Market Mosaic, where I gauge the stock market’s next move by looking at macro, technicals, and market internals. I’ll also highlight trade ideas using this analysis.

If you find this content helpful please hit that “like” button, share this post, and become a subscriber to this always free report if you haven’t already done so!

And be sure to check out Mosaic Chart Alerts. It’s a midweek update covering chart setups among long and short trade ideas in the stock market, along with levels I’m watching.

Now for this week’s issue…

The latest roundup of inflation data revealed a dovish tilt in the Federal Reserve’s preferred measure. But it didn’t generate the expected reaction.

The personal consumption expenditure (PCE) price index rose 2.7% in April compared to a year ago, which matched economist estimates. The 2.8% increase in the core measure that strips out food and energy prices was inline as well.

But the core measure also increased just 0.2% compared to the prior month (orange bar in the chart below), which is the smallest monthly gain so far this year. After jumping into the start of the year, the monthly change in both the headline (blue bar) and core measures are moderating over the past four months as you can see below.

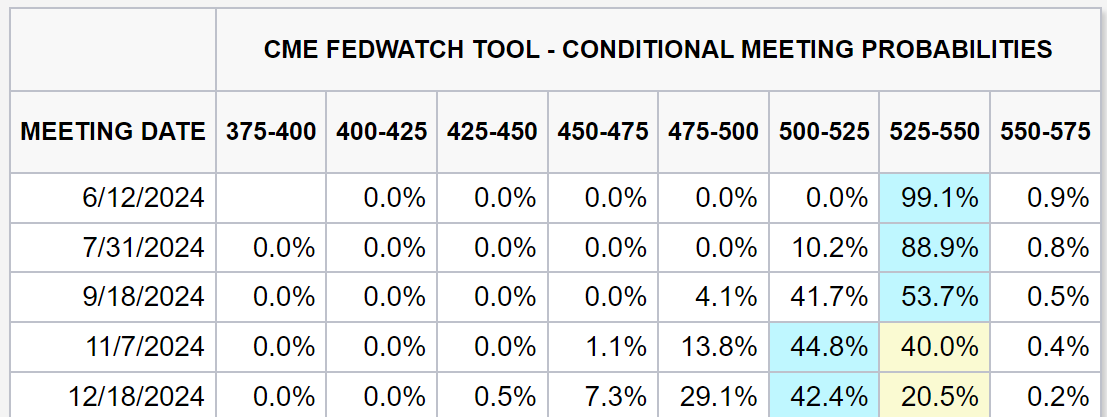

But it’s what didn’t happen in the wake of another inflation report that’s important. Following a brief burst of optimism that more rate cuts could be seen in 2024, that view is shifting back the other way.

Odds for a September cut are a coin flip at 50%, while markets are back to pricing just one 0.25% rate cut in 2024. Not only that, but traders are even recently entertaining the view of another rate hike in 2024 that you can see in the table below.

While the odds for another hike are pretty slim, it goes to show the shifting mindset around the outlook for easier monetary policy. That compares to the start of the year, when odds favored as many as six rate cuts by the Fed.

So despite the seemingly good news contained in the PCE report, other developments on the inflation and economic front are giving investors jitters over the rate outlook.

Even if the Fed does manage to squeeze in one rate cut this year, the central bank looks forced into holding rates higher for longer. Here are the forces driving the shifting outlook for monetary policy, and why it’s not necessarily a bad thing for the stock market.

2 Catalysts Driving “Higher for Longer”

The narrative around “higher for longer” and the outlook for monetary policy has been shifting since last year. The most recent phase of this bull market started last October coincided with a pivot in expectations for several rate cuts in 2024.

But that narrative has been shifting since the start of the year. At the beginning of 2024, markets were pricing six 0.25% rate cuts this year. As you saw in the table above, that figure now stands at just one cut this year. I believe the catalysts that are clouding the outlook for monetary policy comes down to two factors.

First, core inflation remains stubbornly high. While the most recent core measure has fallen to 2.8% compared to 4.8% a year ago, that figure remains well above the Fed’s 2% inflation target.

And its been around that level for five months straight, bouncing between 2.8% and 2.9% since December. That shows progress on disinflation (or a slowing rate of inflation) is stalling out.

At the same time, Fed Chair Jerome Powell unveiled something called the “supercore” measure in late 2022. This measure looks at core services inflation excluding housing, and is a way to monitor inflation pressure linked to wages.

Supercore inflation rose 3.4% in April compared to last year, which is a slightly higher rate compared to the end of 2023 and higher than the core PCE.

Aside from the core and supercore figures, you can also look at the breadth of components in the PCE report running at high levels. The chart below breaks down PCE components into their annual rate of change, with just over 50% of components still running over 3% in the most recent report.

The other catalyst impacting the inflation and interest rate outlook boils down to indicators of economic activity. Despite restrictive monetary policy, the economy is still chugging along just fine.

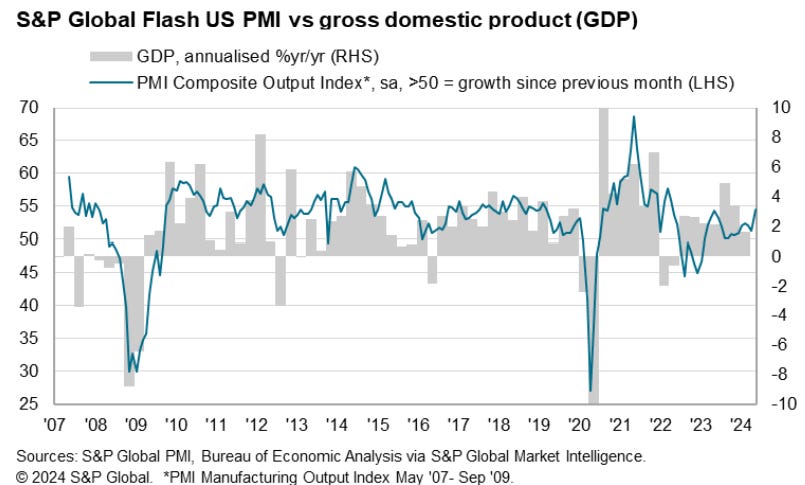

Coincident indicators of activity are actually accelerating, like what you’re seeing with the Purchasing Managers’ Index (PMI) that surveys businesses across the manufacturing and services sector about things like new orders and employment.

They serve as good coincident indicators of activity. While the ISM series is the most popular and will be released this week, S&P maintains their own gauge as well. In their most recent update, S&P’s composite indicator that includes both the manufacturing and services sector rose to 54.4 for the month of May. That’s the highest level in over two years as you can see below with the blue line.

The chart also overlays S&P’s composite indicator with annualized GDP growth (the gray bars). That means current economic activity should bounce back from a weak 1Q GDP report, which echoes the Atlanta Fed’s GDPNow estimate of current quarter GDP growth that’s currently running at 2.7%.

For investors, the concern is that stubbornly high inflation that’s supported by a solid economy will weigh on stock prices via continued restrictive monetary policy and high interest rates. That’s especially the case given the state of stock market valuations, with the S&P 500 trading at a forward price-to-earnings ratio of 20.1 compared to the 30-year average of 16.6.

But a “higher for longer” rate outlook doesn’t have to be a bad thing for the stock market, while the conditions behind monetary policy are also tailwinds for the next round of chart breakouts.

Now What…

Ever since the last rate hike in July 2023, the Fed’s been holding interest rates at the highest level in over 20 years. While investors are concerned that a Fed on hold will pressure the stock market, historical precedent suggests otherwise.

During similar cycles historically when the Fed pauses for an extended period of time, the S&P 500 on average performs well from the time the Fed pauses to the first rate cut as you can see in the chart below.

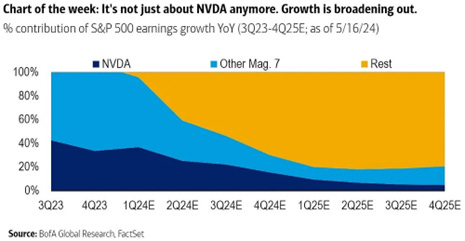

And if a strong economy is part of the reason that the Fed is on hold, that should be a positive catalyst for the earnings outlook. Nvidia’s recent earnings release captured headlines, and has been a huge driver of the S&P 500’s earnings growth in recent quarters along with other members of the Magnificent 7.

But there is evidence that earnings growth is finally broadening out. The chart below shows the contribution to earnings growth in the S&P 500 from Nvidia, other member of the “Mag 7”, and then the rest of the S&P. Based on current estimates, the contribution to S&P earnings growth outside the Mag 7 (orange area) grows to over 50% around the third quarter this year and broadens out further as you can see below.

Finally, combining a strong economy and higher inflation is potent mix to boost commodity prices. Commodities are already known for shining during periods of high and rising inflation. The table below looks at the S&P GSCI commodity index and how it performs during different inflation regimes going back over 50 years. When inflation runs above the Fed’s 2% target, commodities historically deliver double-digit returns annually (chart below).

The weight of the evidence pointing to a strong economy provides another cyclical demand catalyst discussed above. And don’t forget that there’s over $2 trillion in federal spending packages passed over the last three years targeting everything from onshoring key manufacturing industries to overhauling energy infrastructure. Construction spending in the manufacturing sector is running at an annual rate of $223 billion, which is 185% higher than three years ago.

But I don’t want to just guess that inflation and growth catalysts will boost commodity sectors. I also look for evidence via bullish chart setups that prices could be on the move. I already showed you how to do that with copper, gold, and silver several months before their recent gains started accelerating.

Evolving chart setups can tip the next move and provide key levels to watch, which is why I’m closely watching a global metals and mining exchange-traded fund (PICK).

PICK holds mining stocks like Rio Tinto (RIO) and BHP Group (BHP). You can see in the chart below that PICK broke out from a symmetrical triangle pattern back in April. Price tested the upper trendline and then rallied back toward the prior high from 2022. Price is pulling back again, and is finding support at the 50-day moving average while the MACD resets at zero and the RSI finds support at 50. I’m watching if that consolidation can now lead to a breakout to new all-time highs over the $47 level.

That’s all for this week. The coming week will feature several key macro data releases, including more PMI reports along with the payrolls report for the month of May. I’ll be looking for more evidence within those releases that economic activity is accelerating, with confirmation from performance across cyclical and commodity sectors.

I hope you’ve enjoyed The Market Mosaic, and please share this report with your family, friends, coworkers…or anyone that would benefit from an objective look at the stock market.

And make sure you never miss an edition by subscribing here:

For updated charts, market analysis, and other trade ideas, give me a follow on X: @mosaicassetco

And if you have any questions or feedback, feel free to shoot me an email at mosaicassetco@gmail.com

Disclaimer: these are not recommendations and just my thoughts and opinions…do your own due diligence! I may hold a position in the securities mentioned in this report.