The Market Mosaic 10.1.23

S&P 500: So bad it's bullish?

Welcome back to The Market Mosaic, where I gauge the stock market’s next move by looking at macro, technicals, and market internals. I’ll also highlight trade ideas using this analysis.

If you find this content helpful please hit that “like” button, share this post, and become a subscriber to this always free report if you haven’t already done so!

And be sure to check out Mosaic Chart Alerts. It’s a midweek update covering chart setups among long and short trade ideas in the stock market, along with levels I’m watching.

Now for this week’s issue…

With September officially in the books, the month once again lived up to its bad reputation for investors. It’s easily the worst month based on historical return data, with an average decline of 1.2% since 1928.

This time around, the S&P 500 dropped by 4.9% for the month…making it the worst monthly showing for stocks since December. Here’s a chart of the S&P 500’s drawdowns since recovering from 2022’s bear market (h/t to Jim Bianco).

But the most concerning action might be taking place in other corners of the capital markets. Volatile rate markets are wreaking havoc on everything from stocks to housing and fixed income funds.

Just take a look at the 10-year Treasury yield. After breaking out over resistance at 4.34%, it was off to the races. The past week saw the 10-year jump as high as 4.68%, which is the highest level in 16 years.

Higher rates pressure stock valuations by making future corporate profits worth less in today’s dollars. That impact can be felt particularly hard in the growth segments of the market since growth companies expect to generate the bulk of their profits way off in the future. I wrote last week about animal spirits leaving the IWO small-cap growth exchange-traded fund (ETF), and its breakdown from a key pattern.

The S&P 500 has been breaking down as well. First it was the move below the triangle pattern created off the June peak. Now the S&P is close to testing its 200-day moving average (MA – green line) along with the breakout level at 4200 where former resistance could become support.

But amidst the downside in stock prices and rising gloominess of investors, conditions are evolving that could support a rally. Here are a few of the metrics I’m tracking, and why some are so bad it could be good.

Bullish Alignment in Breadth & Sentiment

The S&P 500 is down 6.5% since the July peak, and officially turned in a decline of 3.7% for the third quarter. But the pullback is now creating a combination of conditions that could help spark a rally.

In particular, the intersection of breadth and sentiment at extremes can tip key turning points in the stock market.

Breadth is used to measure participation in a trend, while sentiment indicators can provide contrarian signals when the mood among investors swings too far in one direction. And both are reaching levels last seen at the March lows that helped spark a 19% rally in the S&P 500.

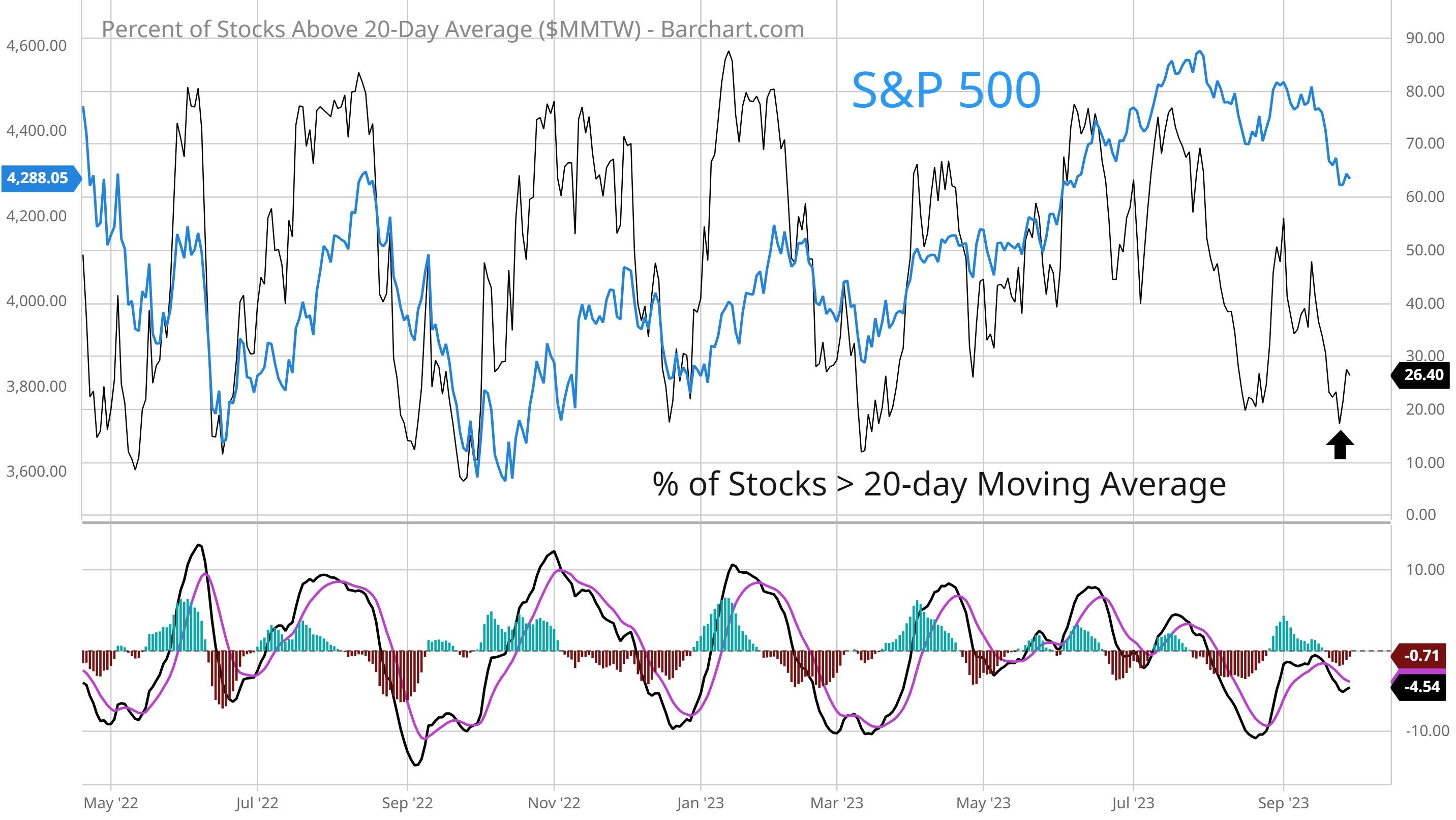

Take breadth for example. Participation in the stock market’s trend is becoming oversold across multiple time frames. That includes the percent of stocks trading above their 20-day moving average (MA) in the chart below.

The metric dipped below the 20% level last week, which is the lowest reading since March and is among the lower threshold seen for this indicator as you can see in the chart.

Extreme values are also being seen in the percent of stocks trading above their 50-day MA. In the post below, I highlighted how bad breadth helped flag the S&P’s poor September performance. But it’s now at one of the most oversold levels of the past three years.

And at the same time, the mood of investors is quick turning extremely bearish. I noted in last week’s market update in Mosaic Chart Alerts how CNN’s Fear & Greed Index entered extreme fear territory for the first time since March. Their metric is comprised of market-based indicators like the volatility index (VIX) and options data.

But you’re also seeing a jump in bearishness among surveys of retail investors. The AAII Investor Sentiment Survey saw bearish investors jump to nearly 41% in last week’s update as you can see in the chart below.

The AAII’s bearish figure is well above the historical average, and is the highest since mid-May when the bank crisis was still unfolding.

Just because investors are growing more fearful and breadth is oversold doesn’t mean stocks have to rally from here. But extremely bearish sentiment coupled with oversold breadth have marked key turning points in the past. Here are clues if a more durable rally can unfold.

Now What…

Should the S&P 500 be able to put together a rally as we head into a favorable seasonal stretch, I’m watching for evidence under the hood that the trend is strengthening.

First, I’m watching for positive divergences among breadth indicators like those discussed above. I’m also tracking the McClellan Oscillator for signs that the average stock is perking back up, which starting to turn higher from an oversold level.

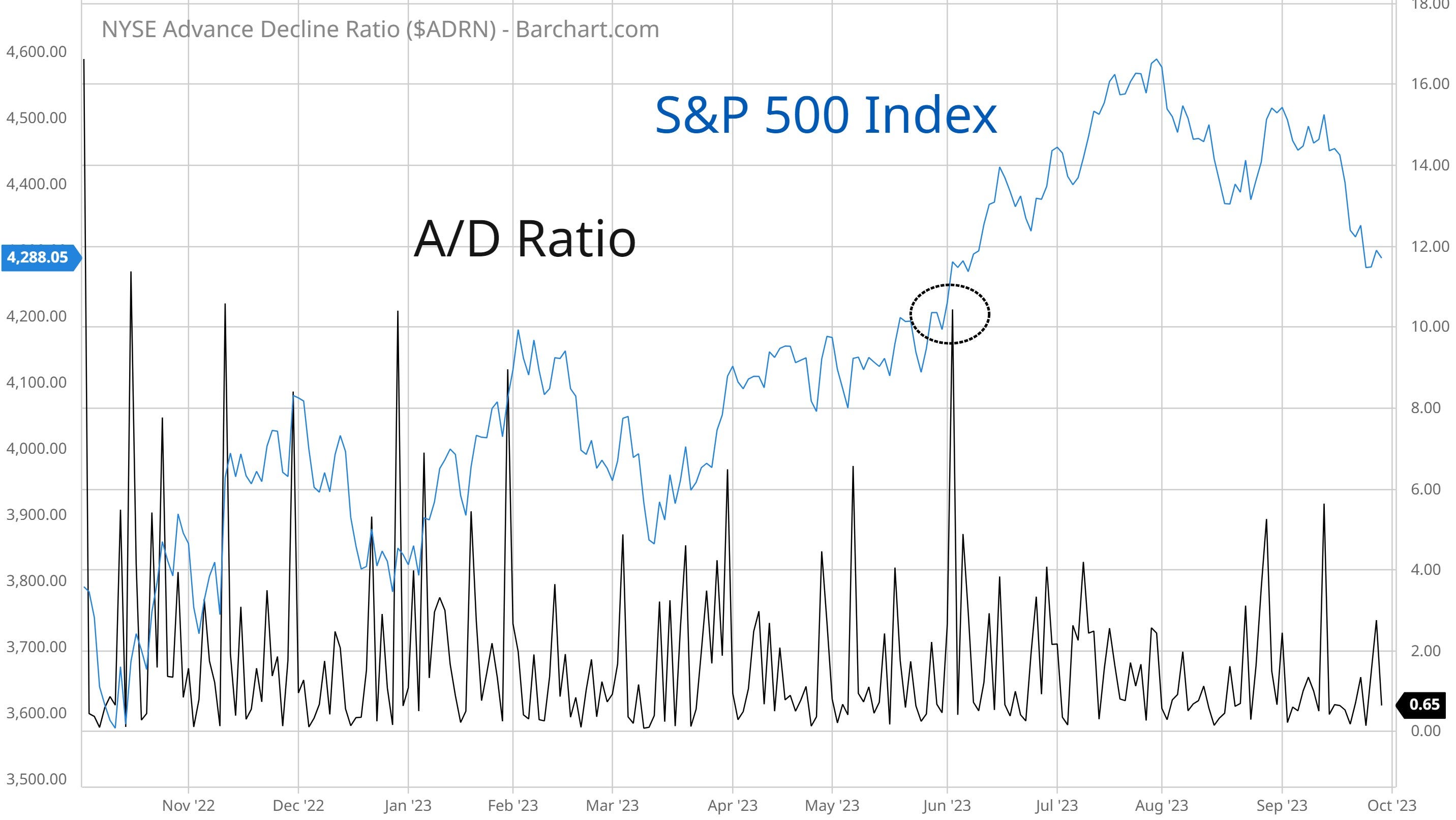

Second, I’m looking for a breadth thrust confirmation. This is a daily surge in advancing stocks relative to declining ones, or in the volume of advancers relative to decliners.

A high ratio can signal the arrival of institutional buyers, whose fund flows will be needed to sustain any rally attempt. The chart below shows the NYSE Advance/Decline ratio, and note the 10/1 figure back in June (circled level on the chart) when the S&P broke out over 4200. That points to strong institutional involvement.

Regardless of what unfolds, I’m tracking potential trades by following relative strength. Much of my focus during recent weeks has been in the energy and commodity space. We’ve continued to see chart setups breakout and hold their gains like the three energy/commodity ETFs that I shared here.

But I’m also noticing trades developing in other corners of the market. If animal spirits can return to the stock market, then IPO bases will be one of my favorite setups to trade. The action in DUOL that went public in 2021 is a great example, which I highlighted in the post below. That action is happening not far below the post-IPO price highs.

That’s all for this week. With news that a stopgap funding bill was approved, the threat of a government shutdown is postponed for another 45 days. So attention will turn back toward incoming economic data and what it means for interest rates and monetary policy. We’ll get the September jobs data and ISM reports this week…just don’t get too distracted by the headlines and miss developments under the stock market’s hood.

I hope you’ve enjoyed The Market Mosaic, and please share this report with your family, friends, coworkers…or anyone that would benefit from an objective look at the stock market.

And make sure you never miss an edition by subscribing here:

For updated charts, market analysis, and other trade ideas, give me a follow on Twitter: @mosaicassetco

And if you have any questions or feedback, feel free to shoot me an email at mosaicassetco@gmail.com

Disclaimer: these are not recommendations and just my thoughts and opinions…do your own due diligence! I may hold a position in the securities mentioned in this report.

Great analysis!!!